30-year Treasury bonds sold at auction on Friday at highest yield in at least 16 years despite Fed’s 100 basis points in rate cuts.

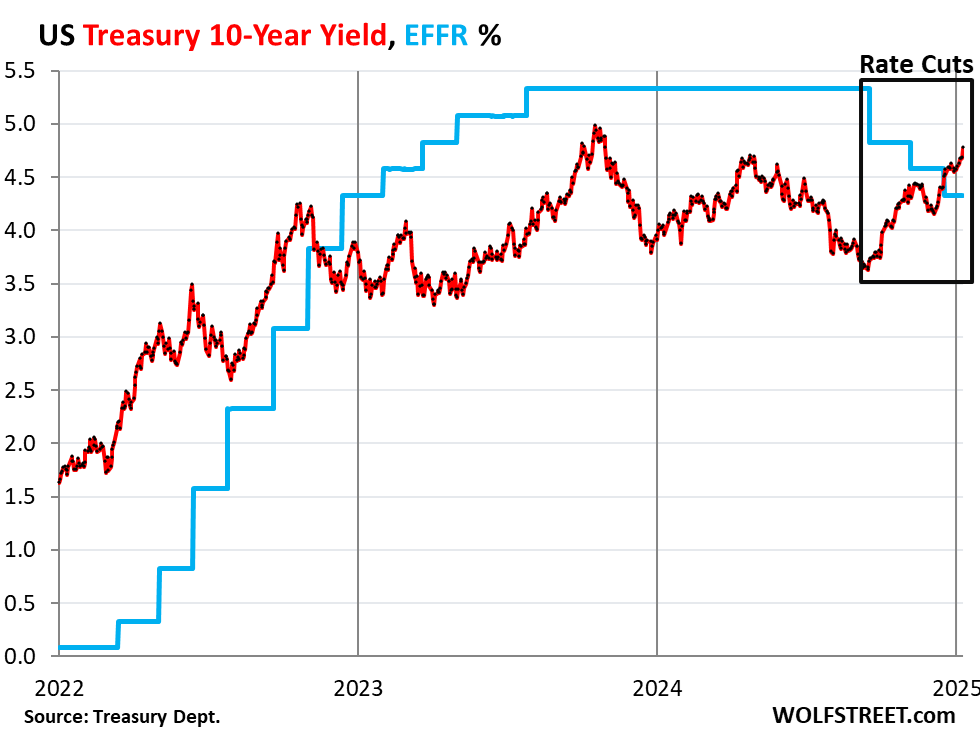

Since the Fed’s 100 basis points in rate cuts, the 10-year Treasury yield has risen by 114 basis points, including by 9 basis points on Friday, to 4.77%, the highest since November 2023, upon news of a continued solid labor market in an economy that is growing substantially faster than the 15-year average growth rate, with inflation re-accelerating in the wings. And seeing these upside risks to inflation, the Fed is gingerly shifting back into its wait-and-see mode.

Also on Friday, the 20-year yield rose to 5.04%; the Treasury Department sold 30-year bonds at auction with a yield of 4.91%, the highest auction yield since before the Financial Crisis; and a daily measure of mortgage rates rose to 7.24%.

The Effective Federal Funds Rate (EFFR), which the Fed targets with its policy rates, has remained at 4.33% since the December rate cut, down by 100 basis points from the pre-cut levels (blue). I’m not sure we’ve ever seen anything like this before – a 114-basis-point surge of the 10-year yield while the Fed cut by 100 basis points – but there’s a good reason for it.

The reason for this phenomenon of the Fed cutting by 100 basis points while longer-term yields soar by over 100 basis points is the unusual situation the economy went through, and why the Fed cut rates.

Normally the Fed cuts rates when it sees a recession on the horizon. And the bond market, also seeing a bad economy ahead, begins to send longer-term yields lower.

But this time around, the Fed cut without a recession in sight, with a solid labor market and above average economic growth despite the highest policy rates in decades. It cut by 100 basis points because inflation cooled a lot from 9% in 2022. But it cooled a lot without a steep recession and big job losses, it cooled despite the economy growing at an above-average rate, which is another rarity. It caused major recession predictors that normally work well to produce false positives.

The yield curve un-inverted last year and is steepening nicely.

Short-term yields haven’t really budged since before the December rate cut, which had already been fully priced in at the time. Now there is no more rate cut priced in within the short-term window of those securities before they mature. For example, on Friday, the 3-month yield was 4.32%, same as in the days just before the December rate cut.

But everything from the 2-year yield and longer has risen substantially since the rate cut. This caused the yield curve, which had gracefully un-inverted entirely just before Christmas, to steepen.

The yield curve had inverted in July 2022, when the Fed’s big rate hikes pushed up short-term Treasury yields very fast, but longer-term yields rose more slowly, and so the short-term yields blew past them.

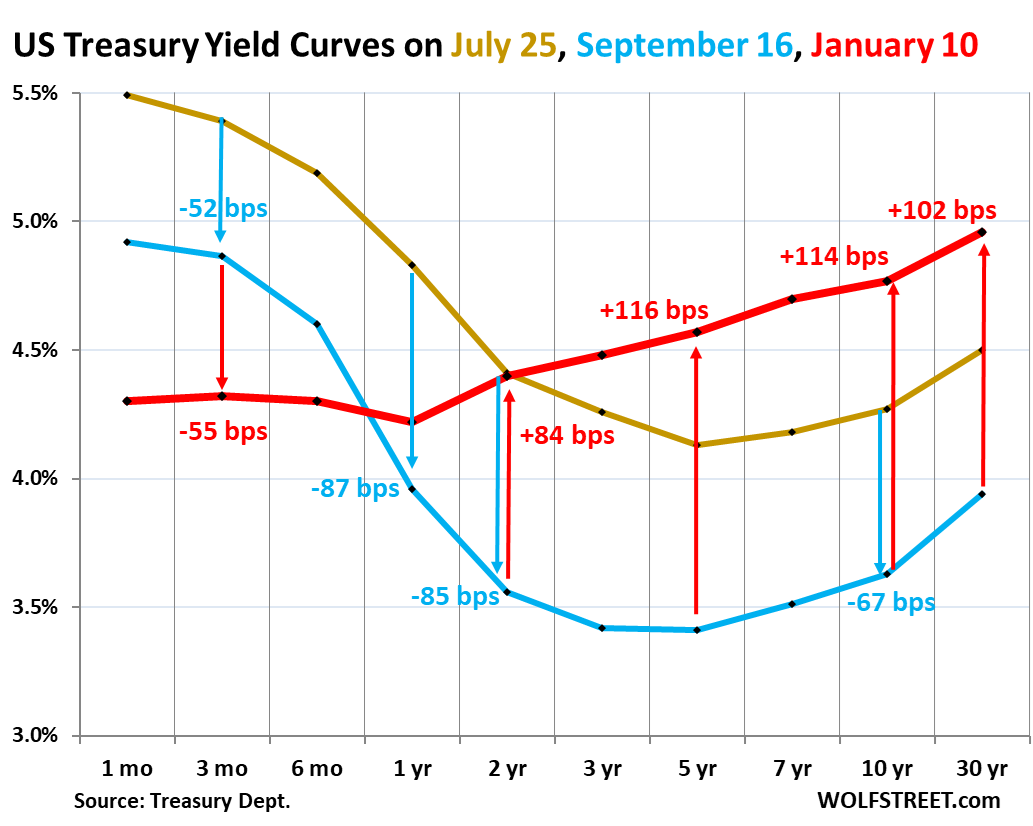

The chart below shows the yield curve of Treasury yields across the maturity spectrum, from 1 month to 30 years, on three key dates:

- Gold: July 25, 2024, before the labor market data spiraled down (which was a false alarm).

- Blue: September 16, 2024, just before the Fed’s rate cuts started.

- Red: Friday, January 10, 2025.

This yield curve is getting closer to looking healthy again, though it remains relatively flat and the steepening process still has some ways to go:

*****

Continue reading this article at Wolf Street.

For more articles like this visit The Prickly Pear.org